Finance for non-finance directors: Part 3

This is the third of three posts summarising some very interesting things I learned about finance on a recent IoD course. In part one I talked about funding and financial statements, in part two I talked about accountancy principles and ratios, and today I will talk about deciding which projects, and which companies, to invest in.

Weighted average cost of capital (WACC)

It was at this point of the course that we got into a lot of acronyms and abbreviations. If you’re less interested in the specifics of project appraisal techniques, scroll down to “Why corporate failure occurs” for how to think about the overall health of a company.

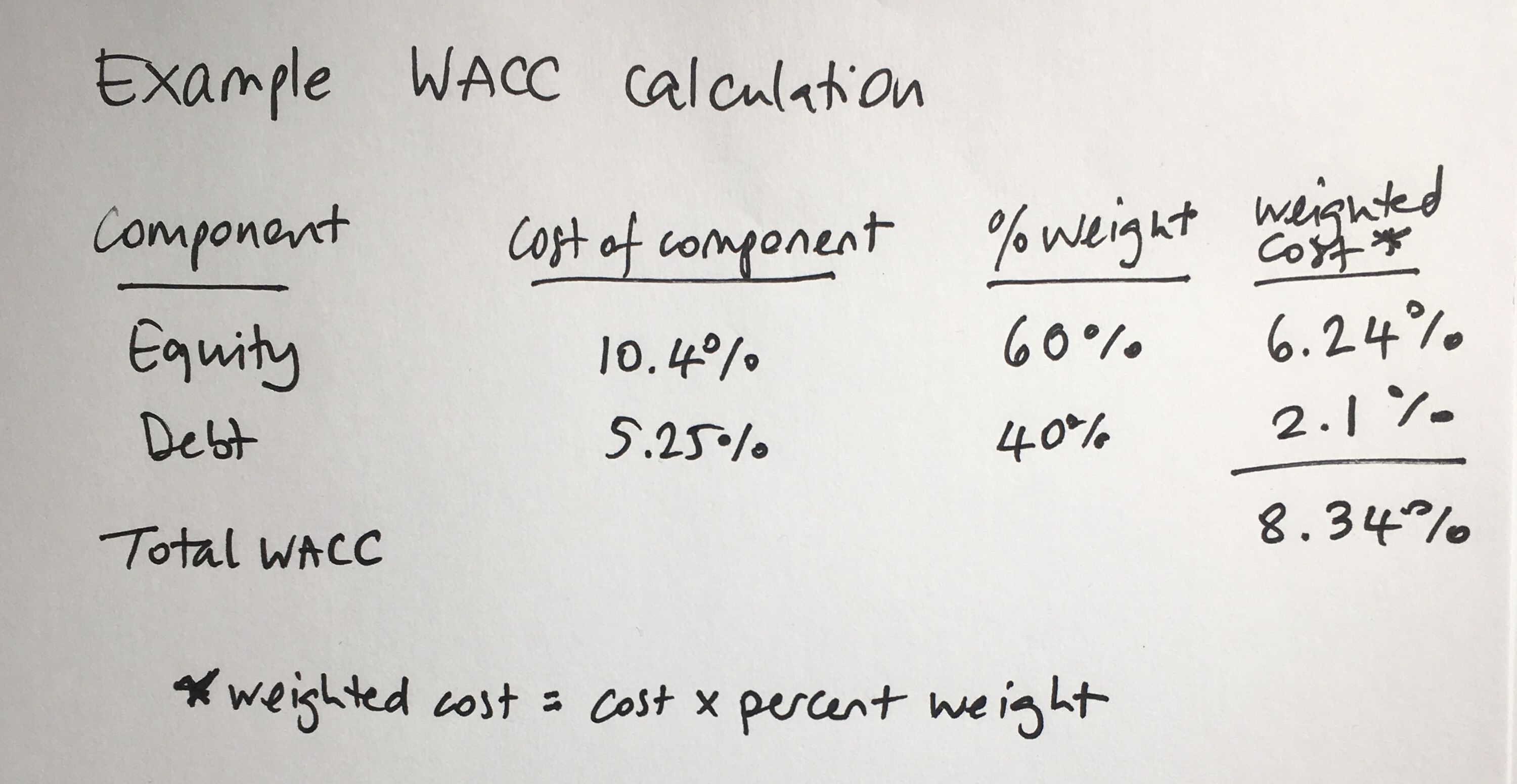

An important acronym for assessing which projects to invest in is the WACC – the weighted average cost of capital.

The point is that capital is not free. For example, debt has interest due on it. The cost of equity is harder to calculate, as technically speaking there is no obligation to pay dividends; but investors will expect a certain return on their investment otherwise they may just sell their shares, so there is a cost to the company associated with equity.

The WACC is calculated by working out the cost of debt and equity, the percentage of funding which is each and summing them.

The WACC is also known as the ‘hurdle rate’, i.e. the minimum return that any project the company undertakes needs to deliver in order to be generating value rater than eroding it. By how much should a capital project or investment exceed WACC? The answer depends on perceptions of the risks involved.

The WACC/hurdle rate is not usually used on its own, but as part of one of the project appraisal techniques that I will talk about a bit more below.

CAPM and beta

A commonly used model to help with calculating the cost of equity is the capital asset pricing model (CAPM), which uses the term ‘beta’ to represent how responsive your business model is to changes in the overall economy. We didn’t learn how to calculate CAPM, but what we learned about beta was interesting.

Beta is represented as whether it is greater than, less than or equal to 1. A beta of 1 means it’s about the same risk as the overall economy. Greater than 1 means higher risk, and less than one means more stable than the overall economy.

For example, airlines are good examples of sectors with a beta higher than 1 – they amplify the risks in the economy. If the economy goes down, people stop taking foreign holidays. Food retail is a good example of a beta lower than 1 – if there is a recession, people do still buy food, and if there is a boom, people do not buy more food.

Risk is something where there is uncertainty of outcome

As I mentioned in the first of these finance posts, risk is not always bad, it’s also an opportunity – and it’s an intrinsic part of doing business. You cannot be a board director if you avoid risk.

You need to know what the principal risks are to the business, and you need to have risk management systems/internal controls in place.

You need to measure risk appetite whenever something major happens.

A risk premium is an extra incentive to investors to take the risk.

Project appraisal techniques

As a director you might have to make a decisions on what project to invest in. Directors need to be able to assess the anticipated returns from a proposal. There are various methods for doing this, and we talked about three:

- Return on capital employed

- Payback

- Discounted cash flow

Return on capital employed asks: what is the return generated as a percentage of the capital outlay?

This is simple, and useful as a screening tool – if it doesn’t exceed the organisation’s hurdle rate (the WACC) it can be rejected. However, the downside is that it’s simple and doesn’t take into considerations cash flow, timing or risk.

Payback asks: how long does it take for the capital outlay to be repaid from the returns generated?

This is also simple, and if the availability of funding or timescale is an issue, it’s very useful. The disadvantages are also with the simplicity – it doesn’t consider total returns over the lifetime of the project, or risk.

Neither of these take into account the ‘time value of money’

Cash today is worth more than cash tomorrow. For example:

- opportunity cost (if you get the money now you can invest it and it could be worth more in the future, whereas if you wait this opportunity is lost)

- inflation

- risk (a bird in the hand…)

So money has a value that varies depending when the money is available – the time value of money.

Discounted cash flow is an appraisal technique that takes into account the time value of money

The first thing is to attempt to calculate the value of all the cash flows of the project as a cash amount today – its present value. Then you subtract the outgoing costs from the incoming money and that gives you the net present value (NPV).

There is a calculation to work out the present value using the forecasted cash flow, the ‘discount factor’ (this might be the WACC/hurdle rate), and time. The ‘discount factor’ is based on lots of assumptions and is an estimate, as is the forecasted cash flow; so there are a lot of guesses in working out the discounted cash flow.

Once you’ve made all these estimates and done the calculation, you have the net present value, and if it is positive, the model predicts the investment will generate value.

It is very sensitive and complex, but this does not mean it is more accurate.

It’s worth asking what the impact of changing a variable by a very small amount is, e.g. 25% to 24.5%. This could make the difference between the net present value being positive or negative and therefore whether it looks like the investment will generate or destroy value.

Using internal rate of return (IRR)

OK, so here’s where we really get stuck into the acronyms and abbreviations. I hope you’ve been paying attention (all are defined above)…

IRR is an application of the NPV calculation that gives an insight into the profitability of the project itself. The IRR of a project is calculated by identifying the discount factor that causes the NPV of the project’s cash flows to equal zero.

You can then ask if the IRR exceeds the WACC.

It also allows projects with different initial investments to be ranked against each other.

The key function of a budget is to assess profitability and financial viability

As well as talking about evaluating projects, we also talked about the purpose of having a budget at all.

A budget includes:

- Forecasting

- Planning (control/coordination)

- Communication

- Motivation

- Evaluation

- Assessing and managing risk

Why corporate failure occurs

We then talked about how to evaluate companies, e.g. for investment, but also in order to understand the workings of your own company.

Corporate failure happens when an organisation is no longer able to continue business due to continued losses or lack of liquidity to honour payments as they fall due – or both.

Reasons can include:

- Overtrading

- Fraud

- Poor controls

- Lack of liquidity

- Unmanageable gearing

If you don’t pay in agreed terms of trade, creditors can wind you up, i.e. they can initiate administration. 70-80% of administrations are initiated by creditors, rather than banks.

Company reports are important for understanding companies’ health

Limited companies report annually to Companies House, and anyone can read these reports online, including creditors and potential investors. Accounts, notes to the accounts, and commentary are collectively called the company report and accounts.

The commentary accompanying the accounts should not just be about numbers, they should be about the why, the narrative. What did we hope would happen? What actually happened? So what?

It should cover leading indicators, i.e. do not wait until KPI (key performance indicators) or targets are met to report, but report on how they are going. KPIs themselves should mostly be non-financial, e.g. Customer Satisfaction. And they should be aligned to the strategy – there should be a “golden thread”.

KPIs should show what you are really going for – what will change when that KPI is met. And the narrative should explain why these results are being measured and what value do they bring to decision-making.

"We don't just want to measure our results, we want to measure what drives our results."

- Howard Atkins, Former CFO, Wells Fargo

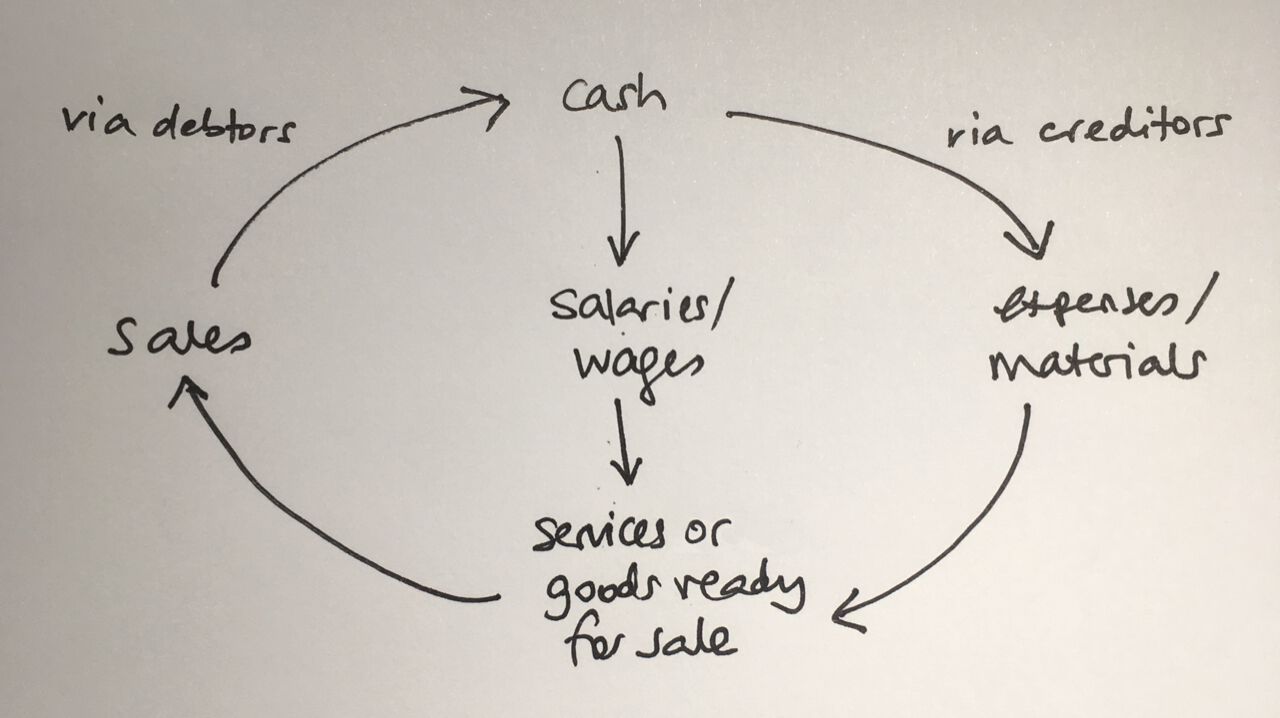

The working capital cycle helps you understand where there may be gaps in funding

Working capital is the capital required to finance the operating cycle of the busness, i.e. pay debts, costs, etc. The working capital cycle is the length of time it takes to convert the working capital into cash.

Understanding this helps you manage your cash flow, inventory, and efficiency, or alternatively, see how well a business you are looking at is managing those things.

How long the cycle takes varies. For example a sandwich takes minutes. Building a ship takes years. Some companies have a negative working capital cycle, for example, you might buy a loaf of bread from the supermarket before they’ve paid the supplier.

The ‘funding gap’ is where there is a difference between collection of payment from your customers and payment of your suppliers. Not just in days, but in terms of money. There are things you can do: move stock faster; reduce payment terms and get paid quicker; delay supplier payment, or fund the gap (i.e. invest money in it).

In a growing business you can expect working capital to be increasing.

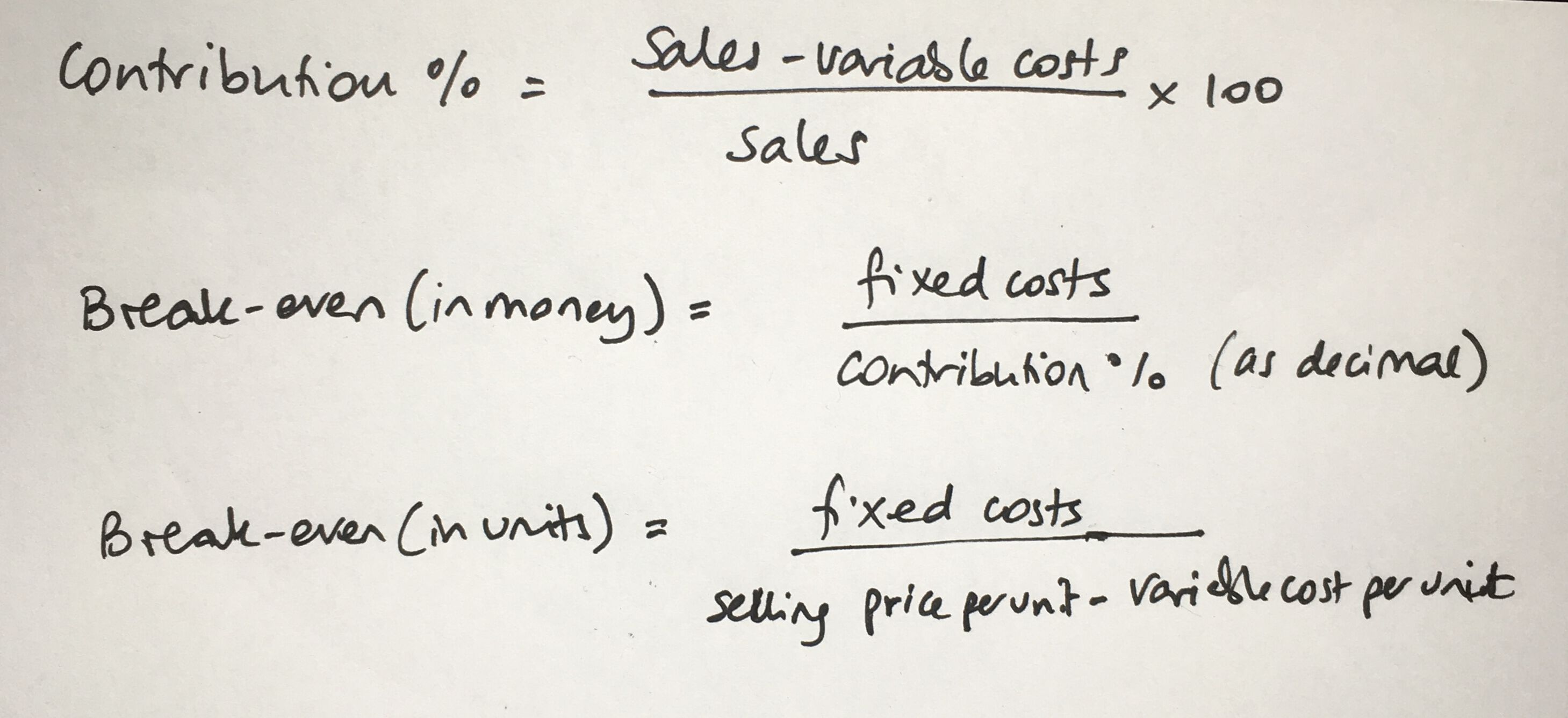

Break-even analysis

A break-even analysis is a really useful tool for understanding how many units the company needs to sell in order to be profitable.

Fixed costs: e.g. salary, rent. These remain constant regardless of activity.

Variable costs: e.g. materials, overtime, sales commission. These vary with activity.

“Contribution” indicates that every time you sell something, it contributes to fixed cost.

The margin of safety indicates how much sales have to drop before you are no longer breaking even. 10% seems high risk. 30% a bit more comfortable.

Fixed costs are useful when thinking about whether you can afford to hire more.

Low operational gearing means low fixed costs and often high variable costs.

High operational gearing means a high level of fixed costs. This is more risky because if there is a downturn, you can’t stop fixed costs.

There are lots of ways of valuing companies

For example:

- Recent similar deals

- Net book value

- Market value/enterprise value

- Earnings multiple/ P/E ratio

- EBITDA

- Free cash flow

None of these are perfect. Share price is just a finger in the air.

The method you choose depends in part on why you are valuing the company. For example, is it deciding whether to invest, or deciding whether to buy the whole enterprise? (In the latter case you have to pay for the shares and pay the company’s debt.)

Is the company balance-sheet driven or P&L driven? Most companies are the latter, but those such as a bank, which uses its capital (i.e. what is on the balance sheet) and lends it out, are termed balance-sheet driven.

Price is what you pay, value is what you get. And valuing is subjective; use the tools with caution and take into account non-financial things (e.g. management credibility).

At this point in the course the instructor brought up a quote from the FT, which she swore was always in the course and wasn’t just because of my presence!

This year, purpose is what investors want to talk about

Companies with a clear purpose that everyone understands are more resilient. The purpose leads to the business model, which leads to strategy and objectives and from there what the principal risks are and what we should be measuring.

Our course instructor recommended The Infinite Game which talks about “the just cause”, i.e. the higher purpose of the company.

The course was incredibly useful and I highly recommend it

I learned so much more on the course than I’ve been able to write up here, but I hope this has given you some useful information.

The main things I took from it were that finance is not cold hard facts, but “it depends”. There are lots of estimates and assumptions, not least in profit, which is not cash. The important question to ask about any financial figure or statement is “so what?”

I’ve learned a lot more about how to evaluate a company and how to read and understand financial statements.

The next piece of the puzzle is tying all this back to the work I actually do; I am a technical director: I and my team are not producing widgets that we can feed into a break-even analysis; we need to understand how our work contributes to the financial health of the company and – possibly more importantly – what work we should not do, because it just does not offer value for money. This course has really helped me understand the structure of what I need to fit my work into; the next piece of the puzzle will follow in due course.

In the meantime, I can now understand the financial pages of the FT!

This is post three of three. You can read part one here and part two here.

If you’d like to be notified when I publish a new post, and possibly receive occasional announcements, sign up to my mailing list: