Finance for non-finance directors: Part 2

On Monday I published part one of three blog posts about finance, finishing with a quiz. In this post I will share the answers to the quiz, then talk about some important accountancy principles and some ways of thinking about the financial health of companies. In part three on Friday, I will talk about methods for evaluating projects and companies.

Answers to the balance sheet quiz

Here are the answers and how we worked them out (there are other ways to work them out, this is just how we got there).

Firstly, we looked at fixed assets and stock. We thought about who might have a large proportion of those and came to the conclusion that Morrisons must be 2, with a lot of physical shops and the largest proportion of inventory. EasyJet must be 5, as they own planes, so 63% seemed about right for fixed assets, plus people pay cash for tickets in advance, so 19% in cash sounds reasonable.

Finally, Apple have some shops and some inventory, so we figured Apple for 1. Our course instructor noted that their balance sheet looks more like one of an investment company. 1 also has the highest level of long-term debt, which matches borrowing to pay a dividend.

Barclays also have a lot of branches, but they are old buildings, so the net book value (the value of a fixed asset after depreciation) is low. It borrows and lends, which correlates with high liabilities and receivables, so that makes 3 look most likely.

Facebook had to be number 6 because of the huge proportion of intangible assets, e.g. acquisition of WhatsApp, and the huge percentage of equity, given that they’ve never paid a dividend.

We thus reached 4 as the IoD by a process of elimination, but the business model of the IoD includes delivering courses (like this one!) which are paid for upfront which matches the high proportion of cash, as well as creditors due in < 1 year.

- Apple

- Morrisons supermarket

- Barclays

- The IoD (Institute of Directors)

- easyJet

Accountancy guidelines

It is mandatory to adopt accountancy guidelines (of which there are a few – IFRS: International Financial Reporting Standards; UK GAAP – UK Generally Accepted Accounting Practice; US GAAP: Generally Accepted Accounting Principles).

However, they are guidelines or principles, not rules. Your accounts do not need to be compliant with every one. If adopting an accounting standard would lead to an outcome that was not true or fair, then you must not follow it. In that case, you would talk to the auditors, who would add a note to this effect.

An important principle is substance over form. Accountants are not lawyers, and the important thing is to communicate fairly and truthfully the state of the company’s finances.

The US guidelines are much more hard and fast, and people try to avoid them; some US companies even base themselves in the UK so as not to have to comply with them.

Following are some accountancy principles and what they mean.

Liquidity is the ability to pay your debts as they fall due

How do you know if there is a problem with liquidity? it depends. What do I owe, when? What am I owed? When will I get it? Will I get it all?

Remember, profit is not cash. Many businesses that make a profit do not have sufficient cash to pay their debts.

Double-entry bookkeeping

This is the commonly used system of accounting where every entry has a corresponding and opposite entry, thereby identifying the two aspects of any financial transaction or adjustment. For example, one entry might show a source of funding (e.g. a sale) and the corresponding entry is the result (e.g. a debtor). When the debtor pays up, that entry would be cash one side and clearing of the debt on the other.

Both sides of each transaction have to add up to the same total. Double-entry bookkeeping is about properly preparing the accounts.

How you pay for things is important

What makes a strategy viable is how you are going to pay for it. Whether you pay now or over time can move something from being viable to non-viable.

Our instructor gave us a case study of a new company that went under because they made a few wrong decisions. 1. They invested some cash when they should have borrowed it, repaying over 10 years, i.e. they should have increased their gearing. And 2. They paid for the first lot of materials in the first month, instead of negotiating 30 days with the supplier. She described this as ‘mismanagement of funding’ and even though they made a profit, the company went under.

Note that in the public sector, the wording is different but the fundamental concepts are the same – you have resources, you need to do the best you can with those resources.

A going concern is a company that will continue trading for 12 months from its annual report

That is, one which has no necessity or intent to cease trading. Necessity could be lack of liquidity, i.e. they will not be able to fulfill their debts when they fall due.

This applies not just at annual report time. If you suspect the company that you are on the board of is not a going concern at any time, you have an obligation to report it – to the board in the first instance. Get it minuted, and get independent legal advice. Knowingly trading while insolvent (unable to meet debts) can lead to directors becoming personally responsible for the company’s debts.

Also note that a lot of things on the balance sheet are valued as if the company is a going concern, e.g. the value of the stock. If you had to sell it off today, it would not fetch as much.

Accruals and matching is about when activities are recognised

I talked briefly about this in the first post. Accruing means we record things when they happen, not when the cash flow happens.

For example, if your financial year is Jan–Dec and you have an electricity bill due next January. By the end of the accounting year you’ve neither received a bill nor paid it, but you have made an accrual to show that the money will be due. You’ve had use of the electricity, you just have not yet paid for it.

Accruals are for both expenses, like the electricity bill, and income, for example if you are due but have not yet received interest, you put the interest in as an an accrual.

Because of accruals, it doesn’t matter to the P&L whether you are paid in advance or after delivery for sales, it will look the same in each case. (However, paid in advance is better – as you will actually have the cash, and therefore will be more likely to survive the year.)

The matching concept only exists in accruals accounting (the alternative to accruals accounting is cash-basis accounting). Matching means you match revenues with the expenses incurred to earn those revenues, and that you report them both at the same time.

The realisation principle

Also called recognition, this is that revenue can only be recognised once the underlying goods or services associated with the revenue have been delivered or rendered.

I understood this as “don’t count your chickens before they are hatched”.

We never realise a profit until it has been earned.

However, we might realise bad news in advance if it is likely to have an impact.

The reliability principle

Requires that there are internal controls for backing up all of this.

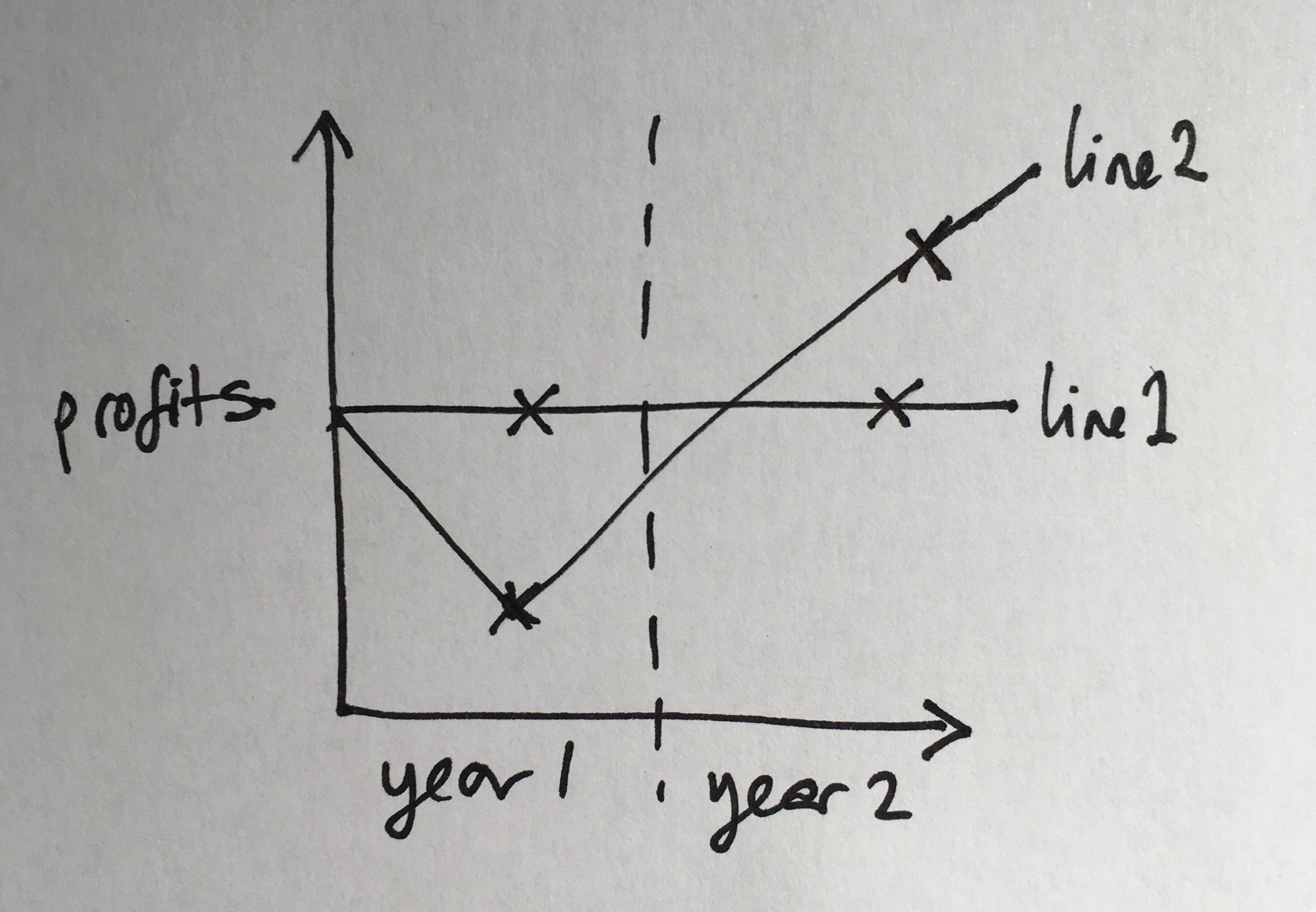

The prudence principle is about making provisions

For example, you might anticipate a significant loss this year, so you charge the P&L, i.e. make a provision. But then, if the loss doesn’t end up happening, in the following year you may ‘release the provisions’. Last year you took a hit to the P&L, but the cash appeared this year – and this year’s P&L goes up.

Our instructor pointed out this is a standard move for a new CEO or Finance Director, as you’ve got a window of opportunity to blame the whole thing on your predecessor. You make provisions in year 1, stating because of everything that was going wrong before you joined, this year you will take a hit on profit. Then in year 2 you release the provisions and it looks great. In fact, the profits may be the same as normal in both years.

In this graph, line 1 and line 2 may actually be the same profit over two years.

You can also make some big write-offs in your first year.

Timing is everything.

Most accounting systems are poor at capturing costs

Every time you interact with a customer it costs money. You might find that customers who cause a lot of trouble are actually causing a loss.

There are rules of thumb; for example it might be that 50% of your customers are causing you to break even, a small number are making you a profit and some are causing a loss. You could find that you increase your profits by reducing your sales and being more selective about your customers.

Are your costs delivering value?

Expenses describe something that is giving value – they are not just costs.

So for example, a new CEO might announce they are striking 10% off the cost base. But if it’s not strategic this could very well be a bad move – those costs may be delivering value.

The role of auditors is to say whether the accounts are true and fair

Auditors are not there to say whether the information presented is “correct” or “accurate”, but whether it is “true and fair”.

It’s an independent examination of the accounts and expression of opinion. Are the accounts properly prepared? Are they free from material misstatements?

‘Material’ means relevant, pertinent. i.e. would a difference here change your decision?

Financial ratios can help with assessing the health of a business

When looking at the financial statements, the context is important. Is this an early-stage or a mature business? What are you expecting to see and why? What is the direction of travel over the next 5-10 years?

Another useful tool is the use of financial ratios. Financial ratios are the relationship between two numbers. They don’t give answers, but might highlight areas to look at.

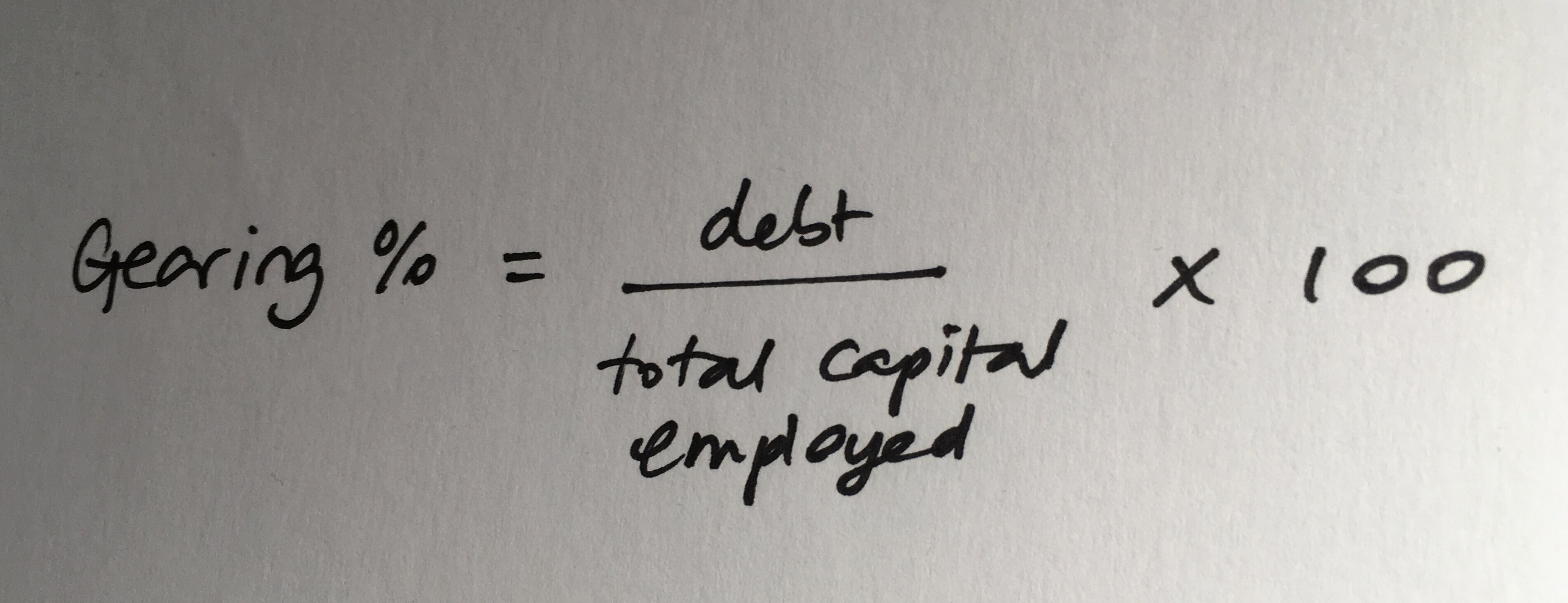

For example, I talked about financial gearing in Monday’s post. The way you calculate the ratio is long-term debt divided by total capital employed (i.e. long-term debt plus equity), then multiply by 100 to give a percentage.

Being highly geared is neither good nor bad; it depends on the circumstances; but it’s a number you can look at to see whether it’s as you would expect for a company in that situation.

Being highly geared is neither good nor bad; it depends on the circumstances; but it’s a number you can look at to see whether it’s as you would expect for a company in that situation.

Other ratios include things like Earnings per Share (EPS), and the Acid-test ratio. Here is a list of some common ratios and here is a list of ratios and their calculations.

It’s worth knowing that there is not only one way of categorising ratios. So for example in my exam for this course, I was told to use the IoD version. As with everything else in accounting the important thing is to be consistent.

Gross profit margin

An interesting ratio to look at is gross profit margin, which is gross profit / net sales. A reminder that profit is an estimate; but even given that we can talk about high margin and low margin businesses.

For example, Waitrose is high margin and Aldi is low margin. Waitrose stores are small. Aldi stores need to be large because if it’s low margin you need to sell more.

Another way of looking at it is that M&S food is mostly perishable, so you can’t stack up lots of it, therefore it needs to be high margin. The percentage of food that is perishable in Aldi is much lower.

If you do different product lines, do not just look at gross profit margin, as profits may be down on some and up on others but the overall line might be fine.

Ratios when thinking about whether to invest in a company

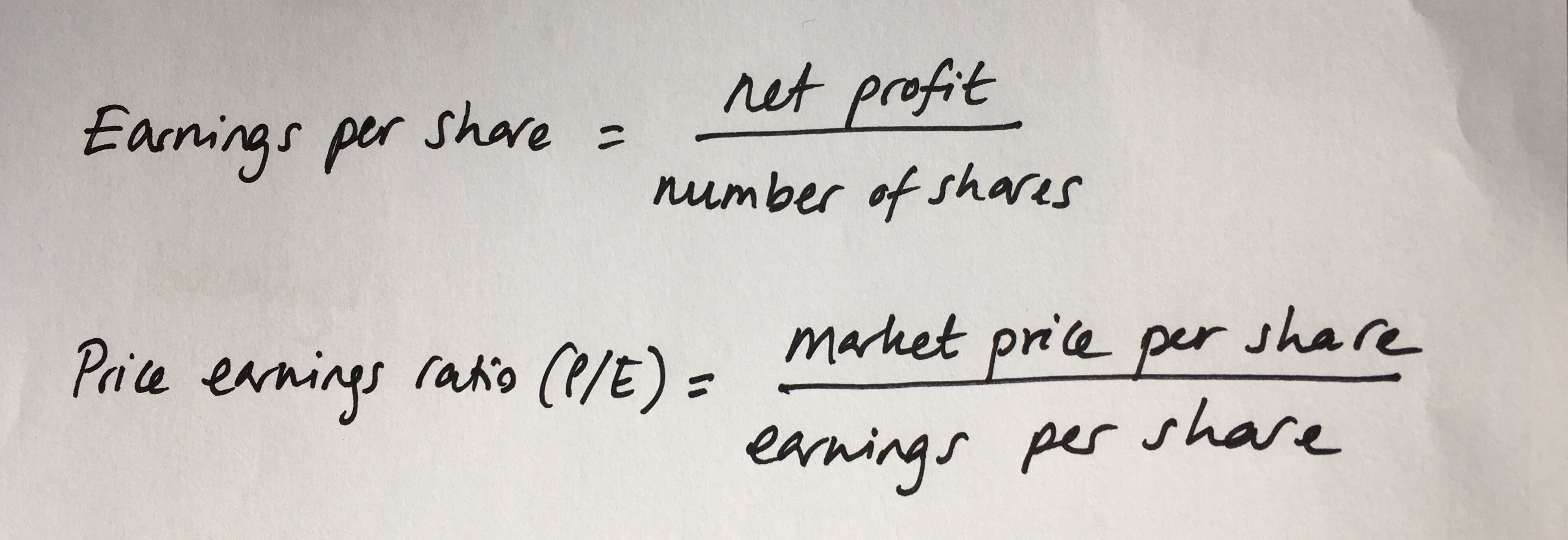

Two of the most commonly used ratios for thinking about investment are earnings per share, and from that, price/earnings ratio (P/E ratio), based on the assumption that the share price represents the discounted value of the future earnings.

You calculate earnings per share by taking profit after tax and dividing by the number of shares. Then the P/E ratio is market price per share over earnings per share. If the P/E for example is 10, then you might say, “the company is trading on a multiple of 10”.

The main reason for trading higher is an expectation that the company might grow in the future (although it could also indicate something like rumours of a takeover).

Evaluating projects and companies will follow on Friday

In this post I’ve talked about some important accounting principles, and some ways to think about the financial health of a business. In the final post on Friday, I will talk about methods for evaluating projects and companies.

This is post two of three posts. You can read part one here and part three here.

If you’d like to be notified when I publish a new post, and possibly receive occasional announcements, sign up to my mailing list: